The current tightening of monetary policy is undoubtedly having an impact. While it may take some time for the slowing of inflation to flow through to the official CPI figures – especially given the level of inflation that is being imported – the economy is set to slow drastically.

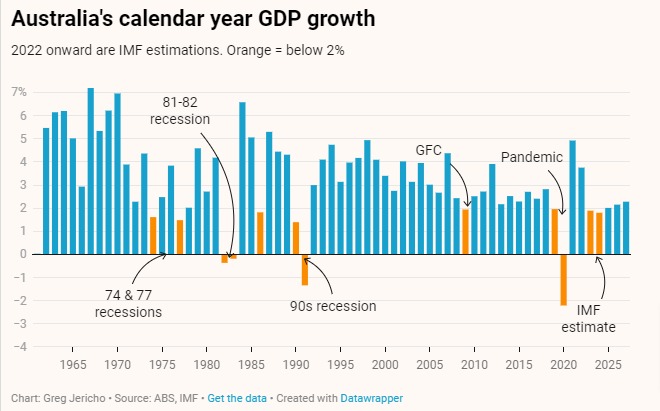

As Labor Market and Fiscal Policy Director Greg Jericho notes in his Guardian Australia column the Reserve Bank in last week’s Statement on Monetary Policy, has forecast GDP growth to slow to levels normally associated with recessions – even if the RBA is not actually forecasting a recession.

However, in one area the RBA is not hedging at all – that of real household disposable income. This measure, which essentially examines the living standards of the average household, is forecast to decline at a pace as bad as any experienced in the past 60 years.

While a fall in household incomes was always expected given the abnormal level of stimulus that occurred during the pandemic, the fall is predicted to be much greater than just going back to where we were. The Reserve Bank predict incomes will fall well below the pre-pandemic trend level.

That such a drastic fall has received little coverage highlights that the orthodox commentary and debate around the economy largely focuses on aspects that minimise workers and households in place of corporations and the “broader” economy of GDP.

The cost of taming inflation is too often discussed in terms of whether it will send the economy into a recession, without examining if that measure misses the real-life experience of most people.

If the RBA forecast comes true, inflation will have been brought back to the RBA target, GDP will have kept growing, but household living standards will have plunged.

You might also like

Want to lift workers’ productivity? Let’s start with their bosses

Business representatives sit down today with government and others to talk about productivity. Who, according to those business representatives, will need to change the way they do things?

A smooth move or a tough transition? Protecting workers who’ll lose their jobs when the Eraring Power Station closes

The Centre for Future Work at The Australia Institute has urged the federal government to take charge of transitioning hundreds of workers into secure employment when the Eraring Power Station shuts down.

Go Home On Time Day 2025. As full timers disconnect, part timers are doing more unpaid overtime

New research by the Centre for Future Work at The Australia Institute has revealed a disturbing new twist when it comes to unpaid overtime in Australia.