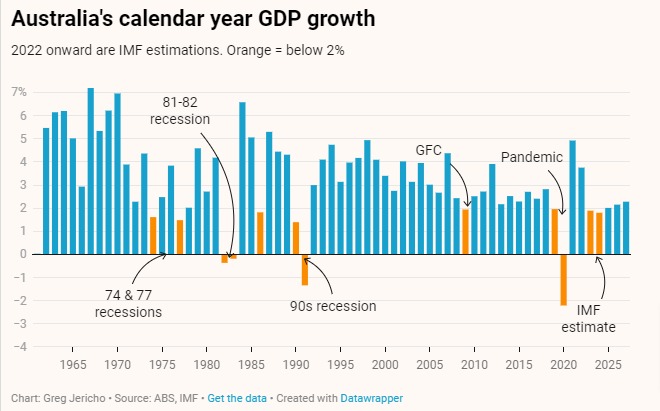

The latest economic outlook from the OECD highlights the precarious path for Australia over the next few years.

As Labour market and Fiscal Policy Director, Greg Jericho, notes in in his Guardian Australia column, the OECD predicts in both 2023 and 2024 Australia’s economy will grow by less than 2%. In the past such weak growth has been associated with recessions. And while a recession is not predicted, unlike for the UK and Germany, the OECD also notes the risks that lie ahead.

One major problem is that most nations around the world are lifting interest rates to attempt to slow their economies and thus reduce inflation. The OECD notes however that when nations act in concert the impact of higher interest rates on slowing the economy is greater, while the impact on slowing inflation is weaker.

Given Australia has a higher proportion of mortgage holders with variable rates this increases the risk that higher interest rates will slow our economy more than in other nations, and still have less impact on inflation.

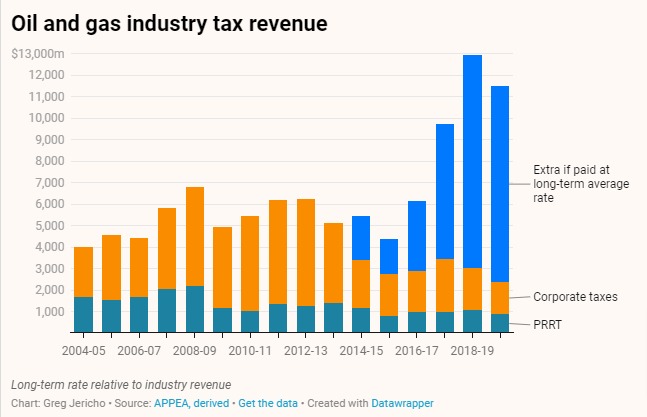

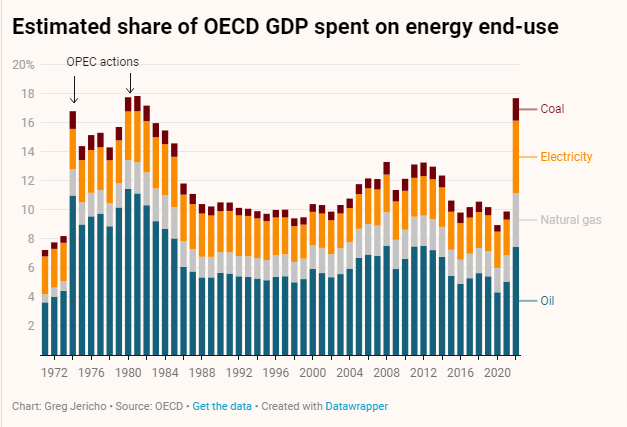

But one sector of the economy are rejoicing at the current conditions that are causing the rising inflation – energy companies.

The OECD notes that the share of GDP being spent on energy by OECD nations is higher now than it was during the OPEC crisis in 1974 and 1980. The evidence again is clear that a windfall profits tax should be levied on coal, oil and gas companies who a reaping massive profits while the cost of living rises sharply for households.

You might also like

Australia’s Gas Use On The Slide

The Federal Government has released a new report that includes projections of how much gas Australia is set to use over the coming decades. There is no ambiguity in its message: Australia reached peak gas years ago, and it’s all downhill from here:

Dutton’s nuclear push will cost renewable jobs

Dutton’s nuclear push will cost renewable jobs As Australia’s federal election campaign has finally begun, opposition leader Peter Dutton’s proposal to spend hundreds of billions in public money to build seven nuclear power plants across the country has been carefully scrutinized. The technological unfeasibility, staggering cost, and scant detail of the Coalition’s nuclear proposal have

A smooth move or a tough transition? Protecting workers who’ll lose their jobs when the Eraring Power Station closes

The Centre for Future Work at The Australia Institute has urged the federal government to take charge of transitioning hundreds of workers into secure employment when the Eraring Power Station shuts down.