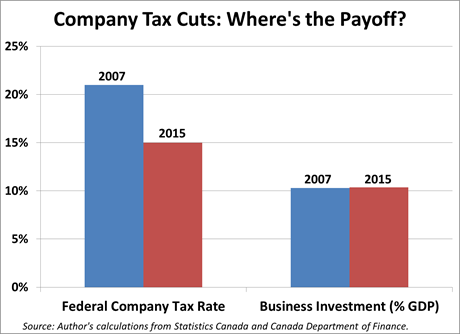

State Income Taxes Would Promote Inequality and Debt

Share

The latest “big idea” on tax policy from the Coalition government is to grant independent income tax powers to the states. This would be accompanied by a devolution of funding responsibility for big-ticket services like health care, hospitals, and schools. Prime Minister Turnbull argues that forcing state governments to raise the money they spend will lead to more accountability and efficiency in public service delivery. And it’s a politically convenient response to the demands from states for more revenues: “If you need it so much, go out and raise it yourself.”

While this trial balloon serves a short-run political function for a government struggling to define its agenda, it would be a terrible way to organize long-run fiscal affairs in a diverse, federal country. Canada’s experience with tax devolution is an appropriate cautionary tale. Like Australia, Canada is a federal country with a complex division of government responsibilities, a vast resource-dependent economy, and big economic and social gaps between regions.

Canada’s ten provinces have the power to set their own personal income and company taxes. They also set province-specific GST rates. The result is enormous variation in tax rates (and rules). Top marginal provincial income tax rates range from 11.25 percent in Alberta, to over 25 percent in Quebec and New Brunswick. Provincial GST rates range from zero in Alberta, to almost 10 percent in Quebec. In each case, provincial taxes are in addition to those levied by the federal government (with its own GST of 5 percent, and a top marginal federal income tax of 33 percent). Each province also sets its own rules regarding coverage, eligible deductions, and tax brackets, complicating inter-provincial business.

It’s not just that individuals must pay tax twice, to different levels of government. (In fact, at tax-filing time, taxpayers must fill out two forms to separately determine what they owe to the federal and provincial governments.) More damaging are the long-run fiscal and social mechanisms set in motion by interprovincial tax disharmony.

Provinces enjoying stronger economic conditions can reduce their tax rates, yet still raise adequate revenue. This sparks a destructive race-to-the-bottom in tax rates that undermines government revenues in all provinces.

The worst example of this occurred during the resource boom of the 2000s. Oil-rich Alberta adopted a low flat-tax applying to all taxpayers (no matter how wealthy). This helped the Conservative government there get reelected. But it exacerbated demands in other provinces (especially neighboring British Columbia and Saskatchewan) to reduce their own taxes in tandem. Well-off Canadians (especially those receiving business or investment income) can easily establish multiple “residences,” allowing them to pay tax in the lowest-rate province.

Smaller, poorer provinces bear the brunt. Consider New Brunswick, in Canada’s poorer east, with a population of just 750,000. Its top marginal income tax rate is more than twice as high as Alberta’s (and New Brunswickers also pay an 8-point GST premium). This makes it all the harder to retain young talent, attract investment, and catch up to the rest of the country. Underfunding provincial schools won’t help economic recovery, either.

By undermining fiscal capacity, tax competition has also contributed to the escalation of provincial debt. Some provinces (like New Brunswick) now owe over 40 percent of their GDP in provincial debt (on top of their share of federal debt, another 33 percent of GDP). Alberta and other higher-income provinces have virtually no debt. Yet indebted provinces pay higher interest rates than Ottawa, resulting in many billions of dollars of avoidable debt service charges. It would be much cheaper for both revenues and debts to be managed centrally, minimizing both tax competition and interest rates.

The Coalition’s most unbelievable claim is that tax devolution will end fiscal squabbles between the governments. That was the theory in Canada in 1977, when the federal government transferred 13.5 percentage points of income tax powers to the provinces, to fund provincially-delivered health and education programs. Forty years later, however, the squabbling is louder than ever. The provinces cannot single-handedly fund public services from their own revenues (especially given the destructive effects of tax competition). So Ottawa still transfers $65 billion per year to the provinces (one-quarter of all federal spending). And debates over those transfers are as intense as ever. Right now, for example, the provinces are furious over a unilateral reduction in federal health transfers.

Federalism is a messy business. And that’s probably how it should be: the whole idea is to ensure a healthy balance between national and regional interests. But the hope that a one-time tax transfer to lower governments can somehow fix all problems of funding and accountability is pure fantasy.

You might also like

6 Reasons to Be Skeptical of Debt-Phobia

In the lead-up to tomorrow’s pre-election Commonwealth budget, much has been written about the need to quickly eliminate the government’s deficit, and reduce its accumulated debt. The standard shibboleths are being liberally invoked: government must face hard truths and learn to live within its means; government must balance its budget (just like households do); debt-raters will punish us for our profligacy; and more. Pumping up fear of government debt is always an essential step in preparing the public to accept cutbacks in essential public services. And with Australians heading to the polls, the tough-love imagery serves another function: instilling fear that a change in government, at such a fragile time, would threaten the “stability” of Australia’s economy.

Commonwealth Budget 2025-2026: Our analysis

The Centre for Future Work’s research team has analysed the Commonwealth Government’s budget, focusing on key areas for workers, working lives, and labour markets. As expected with a Federal election looming, the budget is not a horror one of austerity. However, the 2025-2026 budget is characterised by the absence of any significant initiatives. There is

Feeling hopeless? You’re not alone. The untold story behind Australia’s plummeting standard of living

A new report on Australia’s standard of living has found that low real wages, underfunded public services and skyrocketing prices have left many families experiencing hardship and hopelessness.