The Continuing Irrelevance of Minimum Wages to Future Inflation

Author

Media release

The continuing irrelevance of minimum wages to future inflation

Updated analysis by the by the Centre for Future Work at the Australia Institute reveals that a fair and appropriate increase to the minimum wage, and accompanying increases to award rates, would not have a significant effect on inflation. The analysis examines the correlation between minimum wage increases and inflation going back to 1990, and finds no consistent link between minimum wage increases and inflation. It also reveals that such an increase to award wages could be met with only a small reduction in profit margins.

The report, authored by Greg Jericho, based on previous work by both he and Jim Stanford finds that an increase to the National Minimum Wage and award wages of between 5.8% and 9.2% in the Fair Work Commission’s Annual Wage Review, due in June, is required to restore the real buying power of low-paid workers to pre-pandemic trends. The report also finds that this would not significantly affect headline inflation.

Key findings of the report include:

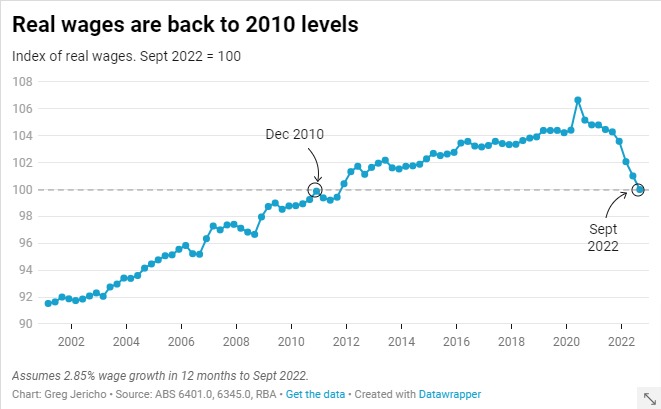

- Last year’s decision, which lifted the minimum wage and award wages by 3.75 per cent, offset the inflation of the previous year but still left those on Modern Awards with real earnings below what they were in 2020.

- By June this year, the real value of Modern Award wages will be almost 4 per cent below what they were in September 2020

- Despite increases in the minimum wage over the past 2 years above inflation, inflation fell by a combined 4.5 percentage points.

- There has been no significant correlation between rises in the minimum wage and inflation since 1990.

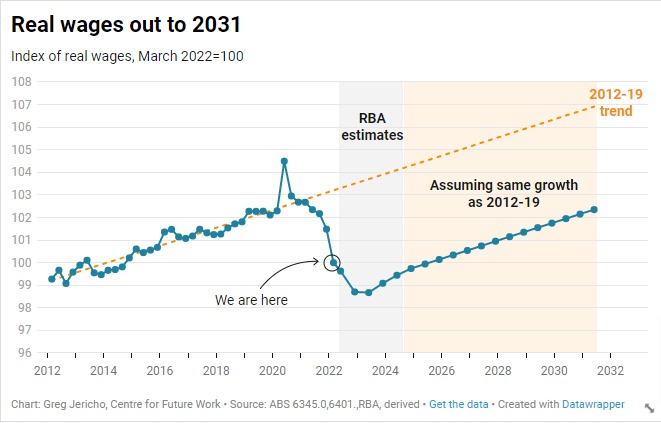

- Raising wages by 5.8 to 9.2 per cent this year would offset both recent inflation and restore real wages for award-covered workers to the pre-pandemic trend.

- Even if fully passed on by employers, higher award wages would have no significant impact on economy-wide prices.

- A 9.2 per cent increase in award wages could be fully offset, with no impact on prices at all, by a 1.8 per cent reduction in corporate profits – still leaving profits far above historical levels

“Australia’s lowest paid workers have been hardest hit by inflation over the past 3 years. The price rises of necessities always hurt those on low incomes harder than those on average and high incomes. This analysis shows there is no credible economic reason to deny them a decent pay raise above inflation.” Jericho said.

“It’s vital the Fair Work Commission ensure that the minimum wage not only keeps up with inflation but also returns the value to the real trend of before the pandemic.”

The Continuing Irrelevance of Minimum Wages to Future Inflation

Factsheet

The continuing irrelevance of minimum wages to future inflation